What is Condo Risk Assessment? A Complete Guide

Published January 28, 2026 · Updated February 15, 2026 · 5 min read

What is Condo Risk Assessment?

Condo risk assessment is a comprehensive evaluation of a condominium's structural integrity, financial health, environmental exposure, and regulatory compliance. It produces a standardized risk score from 0 to 100 that helps buyers, sellers, and investors make informed decisions about property value and safety.

The concept became critical after the 2021 Surfside tragedy, when the Champlain Towers South collapse killed 98 people in a building that had known structural issues documented years earlier. Since then, Florida has enacted sweeping legislation requiring condominiums to address structural safety and financial readiness.

Why Risk Assessment Matters in 2026

Florida's SB 4-D law fundamentally changed the condo landscape. Buildings 30 years or older must now complete a Structural Integrity Reserve Study (SIRS) - a comprehensive engineering assessment of the building's condition and a funding plan to address deficiencies. The initial deadline was December 31, 2025, meaning many buildings are now operating under regulatory pressure.

Without a compliant SIRS, condominiums face increasing insurance costs, potential financing restrictions, and mandatory special assessments to fund repairs. For buyers, understanding where a specific building stands on these requirements is no longer optional — it is essential due diligence.

The Five Dimensions of Condo Risk

Professional risk assessments evaluate condominiums across multiple dimensions. Each contributes to the overall risk picture, and understanding them helps you interpret your score.

1. Financial Health

Financial health is the largest component of any condo risk score, typically worth 40 points. This dimension examines whether the HOA has adequate reserve funds to cover maintenance and repairs without requiring emergency special assessments.

Key metrics include the reserve-to-budget ratio (what percentage of the annual budget goes to reserves) and per-unit special assessment amounts. Buildings with underfunded reserves are at significant risk of sudden assessments that can cost unit owners tens of thousands of dollars.

2. SIRS Compliance

The SIRS requirement under SB 4-D is worth up to 30 points in risk scoring. Buildings that have not completed or submitted their Structural Integrity Reserve Study are flagged as non-compliant. This carries cascading consequences including insurance surcharges and potential lender restrictions.

Critical deficiencies identified in a SIRS report further elevate risk. If engineering assessment reveals imminent structural concerns, the building must develop and execute a remediation plan.

3. Age and Coastal Proximity

Building age and distance from the Atlantic Ocean interact as a risk multiplier. Older buildings (40+ years) face accelerated deterioration, particularly when exposed to saltwater corrosion. A 50-year-old building on Miami Beach's oceanfront carries exponentially more structural risk than the same age building 10 miles inland in Kendall or Coral Gables.

This dimension is scored on age brackets and ocean distance tiers. The combined effect can contribute up to 20 points to the overall risk score.

4. Recertification and Violations

Florida requires buildings over 40 years old to undergo milestone recertification inspections. Buildings with overdue recertifications or open code violations from building department inspections receive elevated risk scores in this category, contributing up to 10 points.

Open violations indicate unresolved safety issues that may affect habitability, insurance coverage, and property values.

5. AI Document Analysis

Modern risk assessment platforms leverage artificial intelligence to analyze actual HOA documents — financial statements, insurance certificates, SIRS reports, board meeting minutes, and governance records. This provides insights that public records alone cannot reveal, such as whether reserve fund contributions are truly adequate or whether governance issues could affect decision-making.

How Automated Risk Scoring Works

Automated risk assessment tools like CondoScan combine government data sources with AI document analysis to produce objective scores. The process involves several steps completed in minutes.

First, the system collects data from public records — the county property appraiser, state community associations registry, and building department databases. These provide baseline property information, ownership records, and violation history.

Next, AI analyzes any available HOA documents, extracting financial data, compliance status, and governance signals. This step transforms unstructured documents into structured risk inputs.

Finally, a deterministic scoring algorithm combines all inputs into a 0-100 score with category breakdowns. The algorithm is transparent — each point deduction is traceable to a specific data point.

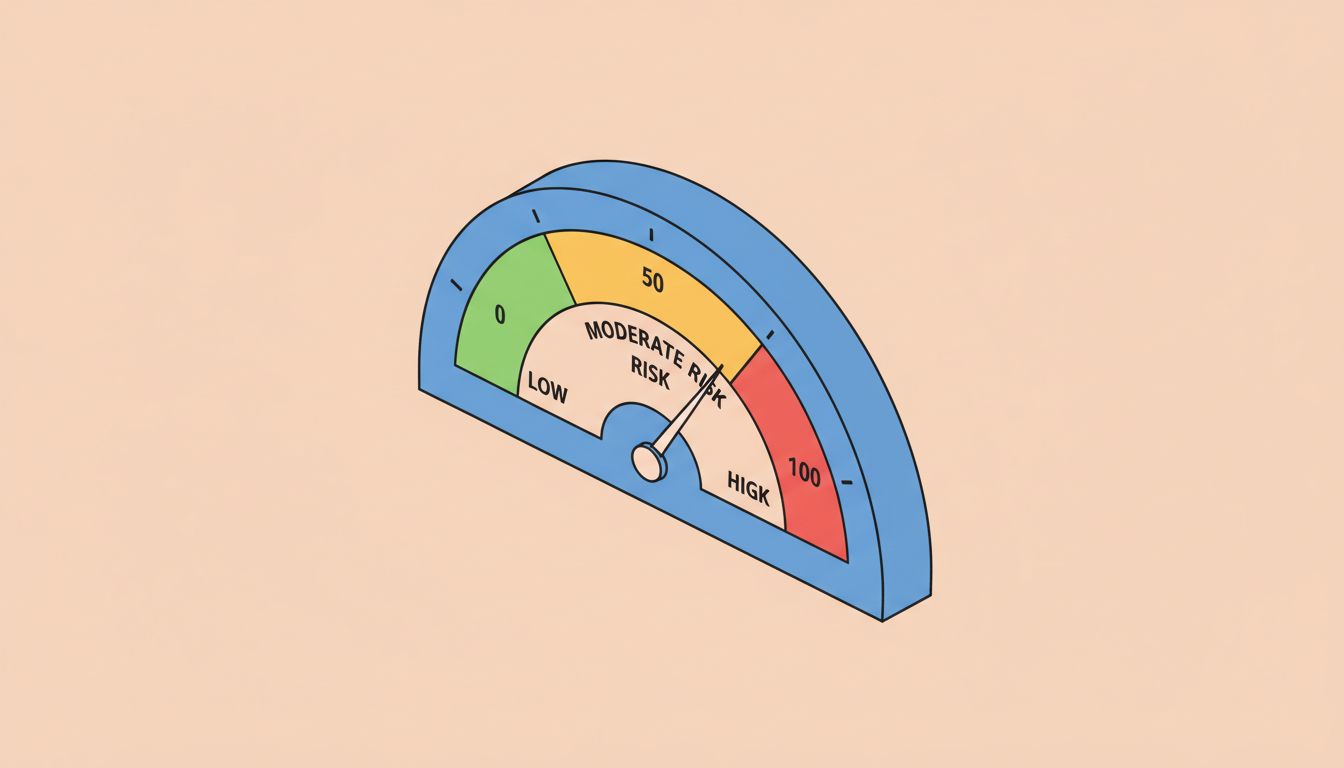

What to Look for in a Risk Score

A score below 30 indicates low risk — the building has strong finances, is compliant with current regulations, and has minimal structural age concerns. Scores between 30 and 59 indicate moderate risk that warrants further investigation. Scores of 60 or above represent high to critical risk requiring careful evaluation before purchase.

Always review the category breakdown, not just the overall number. A building might score well overall but have a critical SIRS compliance gap that could result in significant costs within the next 12 months.

Taking Action on Your Assessment

Understanding your risk score is the first step. From there, buyers should request specific HOA documents to verify findings. Investors should factor risk scores into their acquisition criteria. Current owners should use scores to plan for upcoming assessments and make informed decisions about whether to sell or hold.

For a comprehensive, automated risk assessment of any Miami-Dade condominium, CondoScan provides full reports in under 5 minutes covering all five risk dimensions analyzed above.